Analytics11.09.2022

Monetization of reduction of greenhouse gas emissions in the energy sector

Liliya Zavyalova, Ph.D - international expert for low-carbon development, expert of AvantGarde Group, Uzbekistan

Marina Olshanskaya - Managing partner of AvantGarde Group, Slovakia.

Alexandr Belyi , Ph.D. - Director of AvantGarde Central Asia, Kazakhstan

The declared transition to low- carbon development of the global economy is impossible without the transformation of national energy systems based on the use of fossil fuels into a sustainable and decarbonized system. This implies

the abandonment of the construction of new and the gradual closure of existing power plants, primarily those burning coal and petroleum products. Fossil fuels are being replaced by renewable energy sources (RES) with zero carbon emissions, such as wind, solar energy, hydropower, geothermal energy and biomass. The idea of decarbonizing energy by switching to renewable energy is supported by both the government and the public. In this regard, regulators, investors and consumers are putting increasing pressure on energy companies to reduce their carbon footprint.

It should be noted that in recent years, renewable energy sources have become so cost-effective that they account for most of the new energy generation capacity. Over the past 10 years, prices for solar energy have fallen by about 80%, and for wind energy by 40%. However, in 2022, due to the tense international situation, there was a slight increase in prices for equipment for solar and wind power plants.

Despite the large-scale reduction in prices for solar and wind installations, renewable energy is still losing out to traditional energy in countries with large reserves of fossil fuels and supporting fuel energy, for example, Central Asia countries. Small and medium-sized businesses do not seek to abandon the energy generated at fuel stations in favor of autonomous power supply using, solar stations. The main problem is the large initial investment costs when buying equipment. State benefits, if they exist, do not always solve the problem of investing. Additional sources of funding are needed. A cost-effective tool used by businesses and governments in their low- carbon development strategies has become the setting of carbon price (the introduction of a fee per ton of 2-eq.). Monetization of greenhouse gas (GHG) emissions creates a financial incentive to reduce them.

Before proceeding to the analysis of possible options for monetization of emission reductions obtained during the implementation of carbon offset projects, let's consider the basic information related to the carbon pricing.

1. Basic information about carbon taxes and carbon

Carbon pricing can be direct - carbon taxes, GHG emissions trading systems, carbon credit mechanisms; and indirect - through the introduction of tax on fuel and goods, fuel subsidies. In this publication, only direct carbon pricing will be considered.

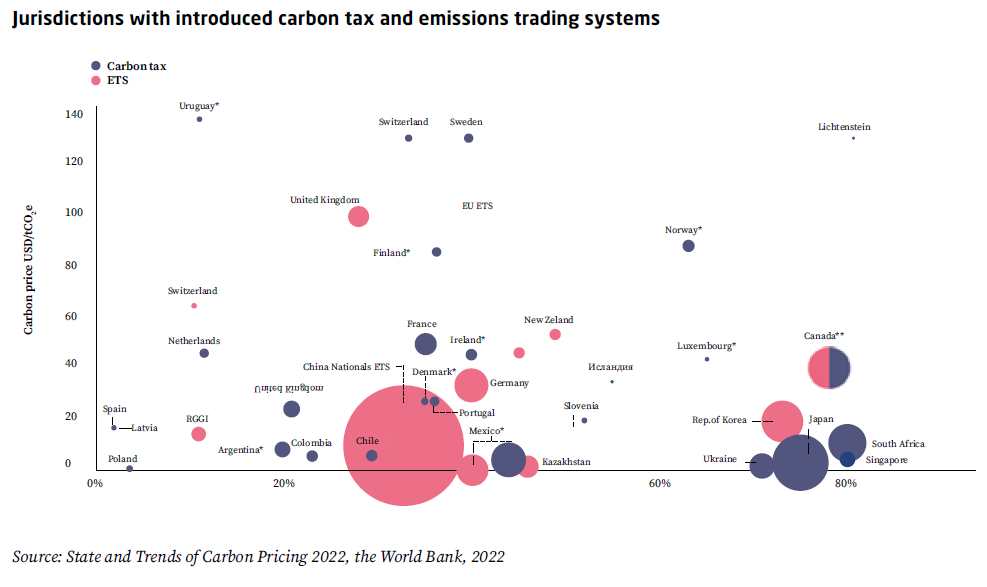

According to the World Bank report "The State and Trends of Carbon Pricing for 2022", there are 64 systems of direct carbon pricing in the world, covering more than 20% of global GHG emissions and generating annual revenue of 53 billion US dollars. Figure shows the jurisdictions (states, regions, provinces, cities) where a carbon tax has been introduced or an emissions trading system is operating (as of 2021).

1.1 Carbon tax

Carbon tax is a fee for burning fossil fuels, typically in the energy and transportation sectors. The price of a carbon tax for each ton of CO2 emissions from burning fuel is set by the government. If the fee for GHG emissions is high enough, then the carbon tax becomes a powerful factor motivating the transition to renewable energy and the introduction of energy-efficient technologies.

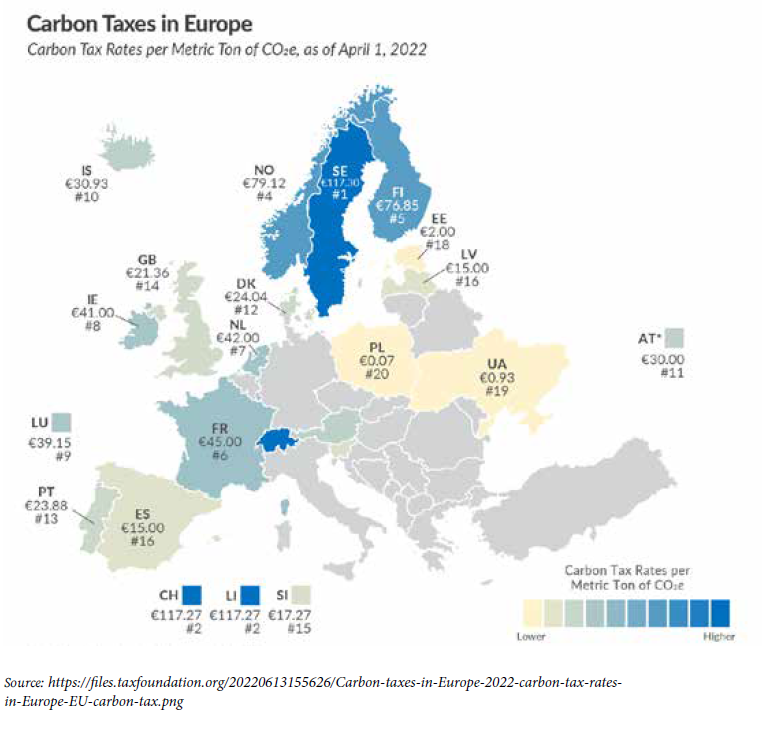

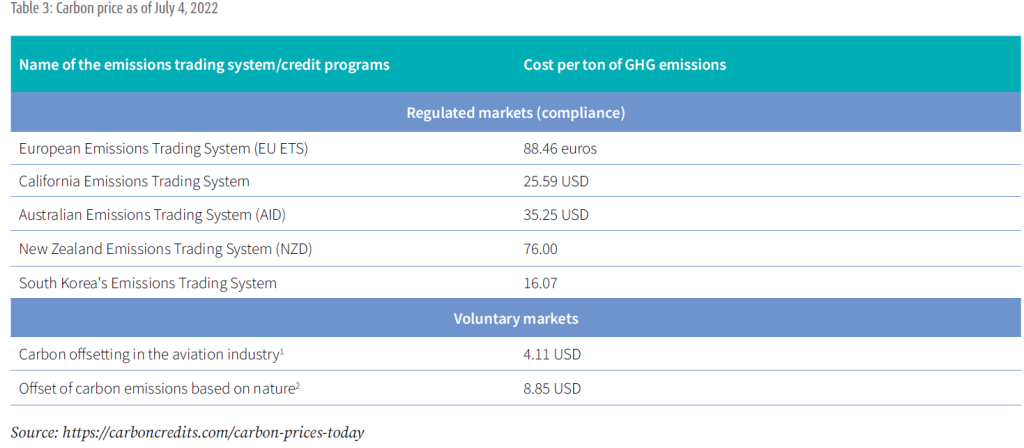

As of 2021, 35 carbon tax programs have been implemented in the world. For example, in British Columbia, the carbon tax has been in effect since 2008. In 2019, South Africa became the first African country to introduce a carbon tax. In 2006, Boulder, Colorado became the first U.S. city with a carbon tax. In 2022, the maximum price per ton with 2-eq. In European countries, the carbon tax was 117.27 euros (Sweden), the minimum was 0.07 euros (Poland).

1.2 Carbon markets

Conditionally, carbon markets can be divided into two main segments: mandatory or regulated (for compliance) emissions trading systems and voluntary - carbon offset programs.

Regulated markets are conditioned by the existence of mandatory GHG emission reduction targets for their participants. Voluntary markets allow companies and individuals to offset their emissions on a voluntary basis by purchasing carbon credits. In practice, there are also hybrid options, for example, through the EU ETS, so-called international credits were also implemented, representing certified emission reductions obtained during the implementation of projects under the Clean Development Mechanism (CDM) and the Joint Implementation (JI) of the Kyoto Protocol. After 2021, the European Commission no longer allows the use of international credits to fulfill obligations under the EU ETS.

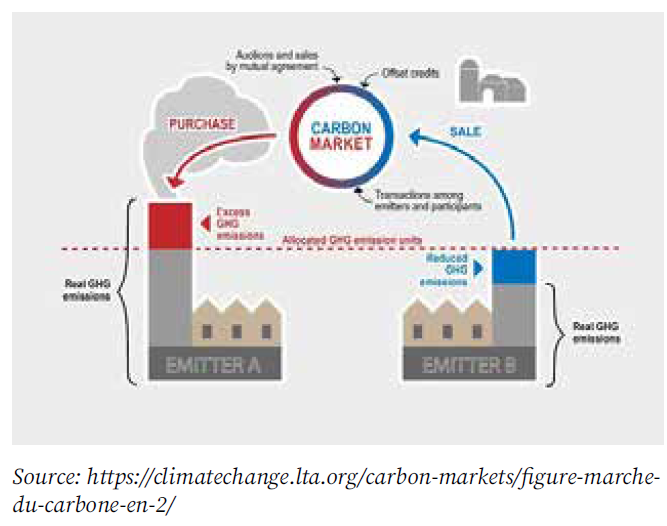

GHG EMISSIONS TRADING (CAP-AND-TRADE GHG EMISSIONS SYSTEM)

The establishment of regulated Emissions trading System (ETS) involves the establishment of a limit on the total amount of GHG emissions in one or more sectors. The total amount of absolute emissions is divided into certificates / allowances /permits for emissions, each of which allows emitting one ton of CO2-eq. Emission quotas are distributed by regulatory authorities between companies free of charge or through an auction. If necessary, companies can buy additional quotas for their own needs or sell excess quotas on the carbon market.

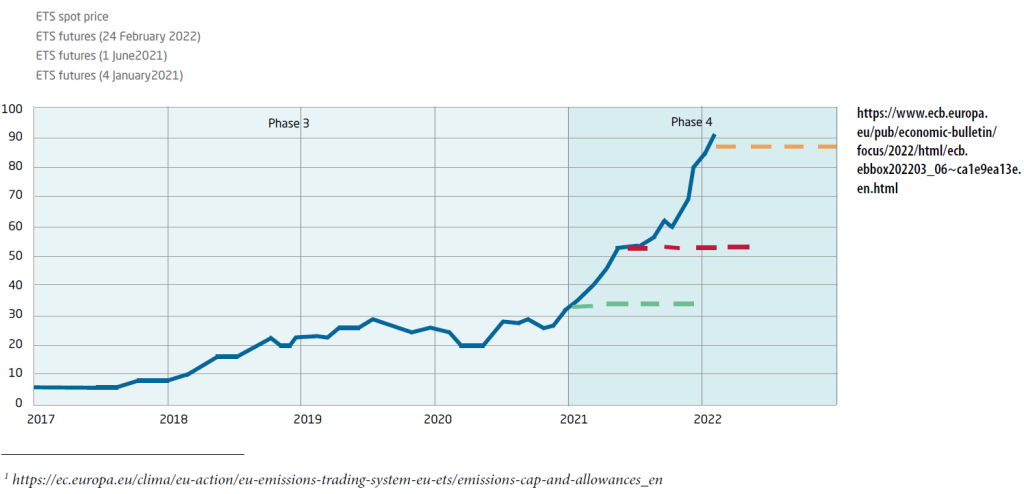

Currently, the largest carbon market in the world is the European Union Emissions Trading System (EU ETS) , operating since 2005. The EU ETS provides for the distribution and trade of GHG emission quotas/permits throughout the EU. Emission permits are set by each Member State and distributed to each facility included in the EU ETS (power plants, industrial enterprises and the aviation sector). It should be noted that the number of emission quotas is decreasing annually (from 2021 - by 2.2%, previously - by 1.7%), forcing the economy to decarbonize.

The price of carbon units in the EU ETS is not set by the government, but is determined by the supply and demand of emission quotas. Since the beginning of 2018, the price of EU emission allowances (EUA) traded in the EU Emissions Trading System has increased from less than 10 euros per metric ton of carbon to more than 90 euros.

It should be noted that the pricing of EU ETS is nevertheless monitored by the regulator in order to avoid defaults, as it was in the 1st and 2nd phases. A Market Stability Reserve (MSR) has been created to increase market stability and reduce excess emissions permits. In the period from 2019 to 2023, the amount of permits placed in reserve will double and amount to 24% of the permits put into circulation.

Since 2011, China has implemented eight regional pilot projects on emissions trading. Since 2017, the national carbon market begins to form, the operational phase of which was launched on February 1, 2021. The market covers more than 2,600 companies in regions with a population of more than 258 million people. Companies specific emissions of which exceed the benchmarks for this type of activity are required to purchase additional quotas on the carbon market.

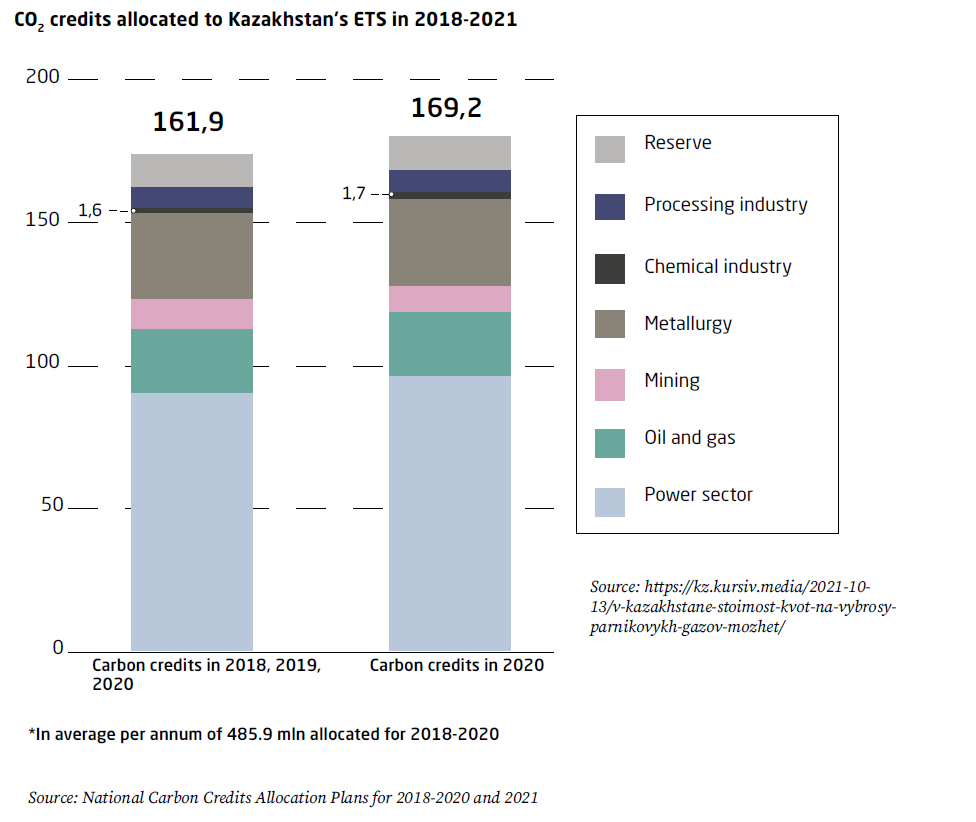

The pilot phase of the Emissions Trading System (ETS) in Kazakhstan was launched in 2013. The ETS covers only CO2 emissions generated by the combustion of fossil fuels (electric power, oil and gas industry), in industrial processes (metallurgy, mining, chemical industry, manufacturing industry), as well as aviation. The emissions trading system includes enterprises with annual emissions exceeding 20,000 tons of CO2/year.

According to the National Energy Report Kazebergy-2021, from 2018 to 2020, 5.6 million tons of CO2 quotas were sold in Kazakhstan's STV, 52 transactions were made.

CARBON CREDIT MECHANISMS

Initially, the fundamental difference between regulated emission trading systems and carbon credit mechanisms was the method of obtaining a "virtual" commodity expressed in tons of CO2. In the first case, the certificate/ permit/quota gives the legal right to emit 1 ton of CO2-eq. In the second case, we are talking about the purchase and sale of emission reduction units or offset credits in tons of CO2-eq received as a result of the implementation of the carbon project.

As a rule, emissions trading systems are regulated by the state, while participation in carbon credit mechanisms is voluntary. Hybrid options include the California Compliance Offset Program (CCOP), which generates carbon offset credits sold on the California ETS. Until 2021, the EU ETS served as a platform for trading international carbon credits (CERs, ERUs) received during the implementation of projects under the Clean Development Mechanism and the Joint Implementation of the Kyoto Protocol.

► INSERT: The term "carbon offset" refers to a reduction in GHG emissions/an increase in GHG effluents used to offset emissions occurring elsewhere. The term "carbon offset credit", or carbon credit/carbon emissions credit, means a certificate used when buying or selling emission reductions per metric ton of CO2 equivalent. The buyer of the offset credit must "cancel" it in order to declare a corresponding reduction in their GHG emissions.

Carbon offsetting credits can be obtained through various activities that reduce GHG gas emissions or increase carbon pickup. For example, a carbon offset project may include:

• Use of renewable energy sources;

• Improving energy efficiency;

• Capture and destruction of highly potent GHGs, such as methane, N2O or HFCs;

• Prevention of deforestation/improvement of land use.

It should be emphasized that any reduction in GHG emissions acquires the status of a compensatory credit only after passing the verification procedure, or obtaining a kind of quality certificate for this "virtual" product.

Voluntary carbon offsetting programs were created by non-governmental organizations (NGOs). As this direction became established , offset programs assumed three main functions:

• Development and approval of standards establishing quality criteria for carbon offset credits;

• Verification of offset projects for compliance with these standards (usually with the help of third-party verifiers);

• Management of registry systems that are put into circulation, transferred from account to account and written off carbon offset credits.

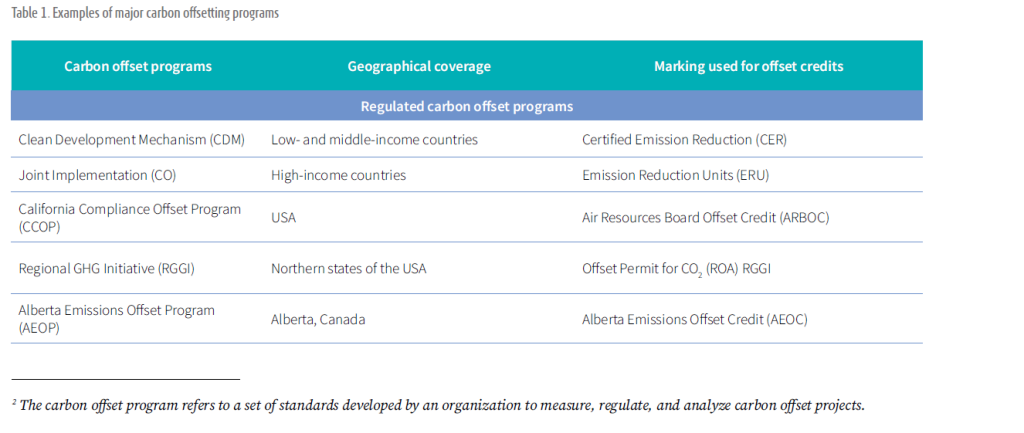

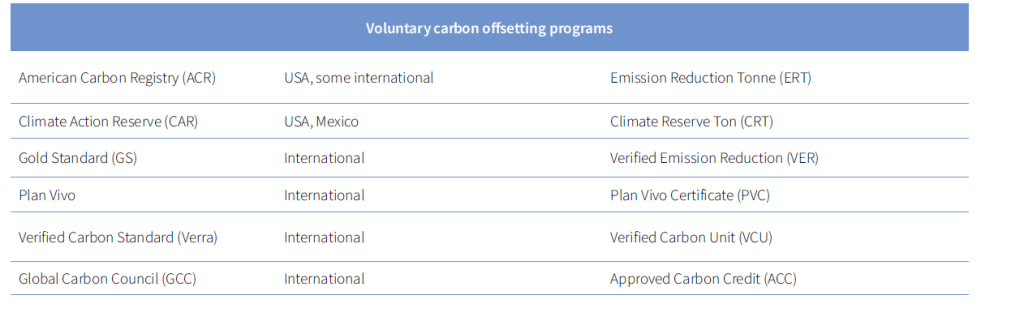

Currently, carbon offsetting programs are often referred to as standards or registries. Each standard issues credits under its own trademark. Table 1 shows the most significant both regulated and voluntary carbon offset programs.

Table 2 shows the four largest carbon offset programs for 2022. Central Asian countries can participate in two of them: the verified Carbon Standard and the Gold Standard.

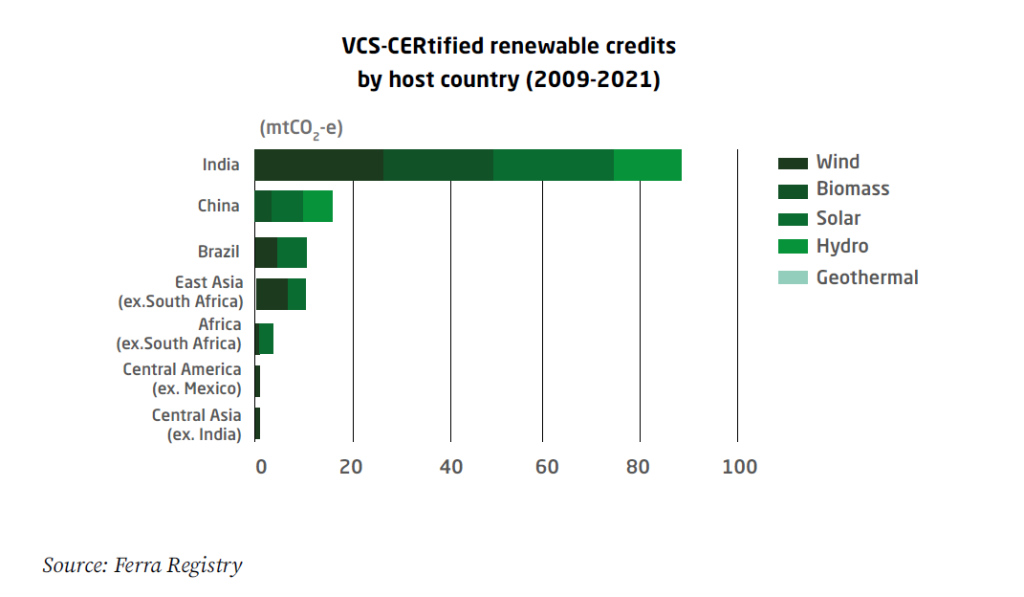

The Verra program has more than 1,806 certified projects with a total reduction/absorption of carbon emissions in the amount of more than 928 million tons of emissions CO2-eq. The projects cover 15 sectors, including renewable energy sources, conservation/restoration of forests and wetlands, improving transport efficiency and etc. The figure below shows the number of carbon credits in the field of renewable energy introduced by Verra in 2009-2021.

Projects registered under the Gold Standard (GS), should provide long-term social, economic and environmental benefits to local communities. As a rule, offsetting projects must contribute to the achievement of at least three of the 17 UN Sustainable Development Goals in order to be certified for their emission reductions.

1.3 "Life cycle" of carbon offset credit

Regardless of the program, there are five main stages on the path of a carbon offset credit, starting with its creation and ending with cancellation.

1) Development of methodology. GHG emission reductions obtained during the implementation of any carbon project become a commodity (offset credit) only after confirmation of its quality or certification. The document defining the project requirements, including the emission calculation algorithm, is a methodology or protocol specific to this type of offset project. Most carbon offset programs have their own libraries of approved methodologies. However, if there is no methodology acceptable for this type of activity, you can develop your own methodology and approve it in the selected program.

2) Development of the project document, validation and registration. The project document is developed in full compliance with the methodology or standard. After validation by an independent company, the project is registered in the selected carbon offset program. The official "registration" means that the project has received approval and has the right to start generating carbon credits.

3) Project implementation, verification and introduction of offset credits into circulation. The implemented project is monitored in accordance with the Monitoring Plan. The generated emission reduction is periodically (usually once a year) verified by an independent verifier. The offset program approves verification reports, and then puts into circulation the amount of carbon offset credits equal to the number of verified GHG emission reductions in CO2 equivalent. Carbon credits are usually deposited to the project developer's account in the registry system administered by the offset program.

4) Transfer of offset credits. Carbon credits put into circulation can be transferred to different accounts in the register of the offset program. Transfers are usually made when buying or exchanging. Buyers can then use the offset credits by writing them off, withholding them, or transferring them to other accounts. Credits can change hands several times (transferring between multiple accounts) before they are deleted and used.

5) Withdrawal of offset credits from circulation. Before using carbon credits, owners must "write them off" in order to declare the associated GHG emissions reductions. Withdrawal from circulation takes place in accordance with the process specified in the register of each carbon offset program. After repayment of the offset credit, it cannot be transferred or used (this means that it has actually been withdrawn from circulation).

1.4 What influences the demand and pricing of carbon credits

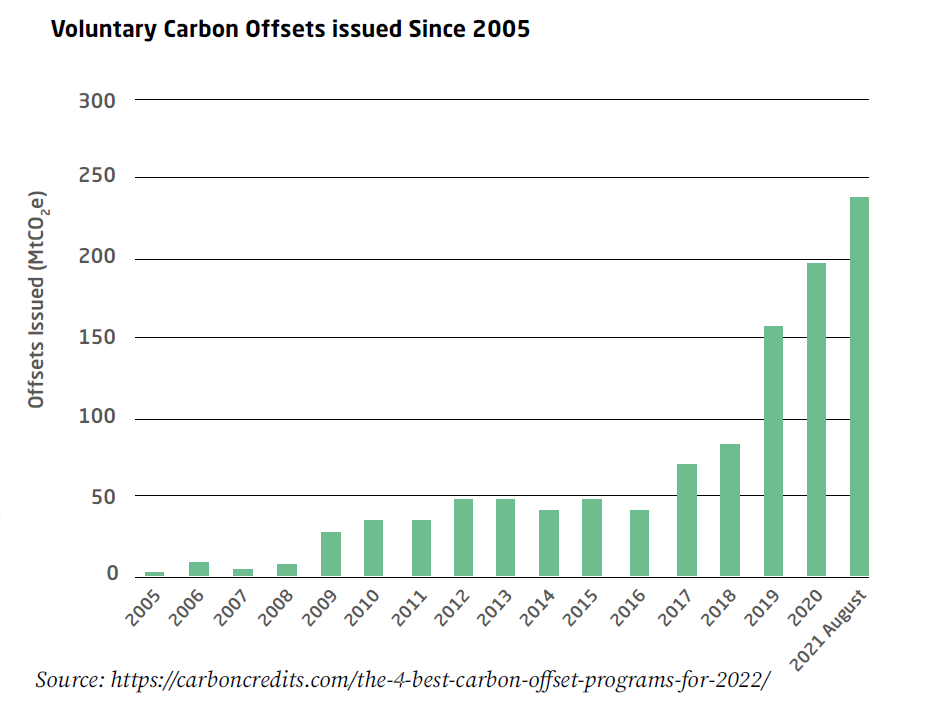

Voluntary commitments of the world's largest companies to decarbonize business served as a kind of trigger in the revival of the voluntary market. Since 2019, there has been a steady increase in the number of carbon credits put into circulation, and in 2021, the volume of transactions on the voluntary market exceeded the volume of transactions in 2020 by 92%.

According to the World Bank's annual report "The State and Trends of Carbon Pricing for 2022", in November 2021, the total value of the voluntary carbon market exceeded $1 billion for the first time. This rapid increase in value reflects both rising prices and growing demand from corporate buyers, which leads to an increase in transaction volumes. According to McKinsey's forecast, the annual demand for carbon credits in the world by 2030 may reach from 1.5 to 2 billion tons of CO2-eq., and by 2050 -up to 7-13 billion tons of CO2-eq4.

International aviation can also be attributed to large consumers of carbon offset credits. In 2016, the International Civil Aviation Organization (ICAO) introduced the "Carbon Offsetting and Reduction Scheme for International Aviation (CORSIA)", according to which by 2027 90% of international flights should be "compensated" with certificates corresponding to CORSIA. In the period from 2021 to 2026, GHG emissions from flights between states voluntarily participating in the pilot phase of CORSIA should be compensated. Volunteer countries cover about 77% of all international aviation activities. From 2027, almost all international flights will be subject to mandatory offset requirements. It is expected that in the period from 2021 to 2035, the demand for offset credits under CORSIA will be from 1.6 to 3.7 billion.

The completion of the Article 6 rulebook of the Paris Agreement will create conditions for increased private sector investment in voluntary carbon offsetting projects.

This growth in demand and the upward trend in prices are attracting investors who are beginning to view carbon credits as an investment product that should bring high returns in the coming years.

Some countries are also starting to think about purchasing carbon credits to fulfill their obligations under the Paris Agreement. In Japan, the Joint Crediting Mechanism (JCM) program has been operating since 2013, acquiring carbon credits in developing countries through partial financing of carbon projects. In 2022, it is planned to expand the number of participants from 17 to 30 or more. The Central Asian States are also considered as potential participants.

THE PRICE OF CARBON CREDITS

The price of carbon offset credits varies in a very wide range from <1 to > 50 US dollars per ton. As with any commodity, the carbon price is determined by supply and demand, and also depends on:

• The type of project that compensates for carbon emissions;

• The carbon standard/program according to which it was developed;

• Associated benefits (environmental, social, economic) associated with the project.

In addition, pricing is influenced by what stages of the "life cycle" of credit a deal on its sale is concluded. As a rule, the nominal price will be the minimum at the conclusion of the transaction at the first stages, the maximum - after receiving a certificate from the carbon offset program.

The World Bank report "The State and Trends of Carbon Pricing for 2022" indicates that in the voluntary market, global average prices for carbon credits increased from US$ 2.49 per ton of CO2-eq. in 2020 to US$ 3.82 per ton of CO2-eq. in 2021.

According to S&P Global Platts, from June 2021 to January 2022, the price of offset credits related to carbon dioxide uptake (tree planting) has more than tripled, from about $4.65 per ton of carbon to about $14.405.

1.5 Sale of carbon credits

There is no global carbon market where all the trade brands related to GHG emissions are represented. Numerous emissions trading systems operate according to the rules established by their own regulator. The unification of all ETS into a single global system is a matter of the future. So far, such an attempt has been made when linking the EU ETS and the Swiss Quota Trading System.

Carbon credits received under voluntary carbon offsetting programs cannot be sold in regulated markets. The platform for trading such compensatory xredits are stock exchanges trading in finished goods (respectively, the price is higher), brokers, retailers, as well as direct purchase through the signing of an Emission Reduction Purchase Agreement (ERPA) at the project development stage. In the latter case, the price will be lower than the market price and depends on how the carbon risks are distributed. The buyer can also bear the costs of developing the project.

2. Practical steps to generate carbon offsetting credits

As discussed above, monetization of carbon emissions is a source of additional income that increases the investment attractiveness of the project. But it should be remembered that in addition to carbon revenues, there are also carbon costs associated with:

• Preparation of PDD and its validation by an independent company;

• Monitoring, including the purchase of measuring equipment, if necessary;

• Verification of emission reductions by an independent company and their introduction into circulation;

• Entering the project and carbon credits into the register, as well as using the register.

Depending on the scale of the project, the average costs for performing all these activities vary from tens to hundreds of thousands of US dollars.

Model estimates have shown that, taking into account any income and a small margin, the minimum price of carbon credits covering the average project costs should be 8.20 euros for energy efficiency projects, 8.10 euros for renewable energy projects and 13 euros for forest management projects6. It means that before making a decision on the implementation of a carbon project, it is necessary to estimate at least approximately the carbon costs and revenues from the sale of emission reductions.

2.1 Standard selection

The first step in the development of any carbon offsetting project is the choice of a standard or program for carbon offsetting, since each of them has its own requirements for the preparation of documentation, including the choice of methodology. There are two main standards in the voluntary market: the Gold Standard (GS), Switzerland, and the Verified Carbon Standard (VCS), USA.

Central Asian countries can register their projects in the registries of the Verified Carbon Standard, the Gold Standard, as well as the Global Carbon Council (GCC), Qatar.

2.2. Preparation of the project document design (PDD)| based on the approved methodology

In the case of a carbon offset project, the preparation of design and technical documentation goes beyond the scope of a standard feasibility study. Additionally, the project document design is being developed, including a description of the baseline and the project, calculation of emissions from the baseline and the project, calculation of emissions reduction, as well as a monitoring plan. When developing a PDD, the methodology recommended by the selected standard for this type of activity should be applied. If there is no appropriate methodology, then it can be developed and approved. However, this option, which is quite time-consuming and expensive, should be used in cases where it is a question of large amounts of emission reduction or the implementation of a number of projects.

In all standards, the project must also meet four requirements:

• Complementarity

• Exclusion of double counting

• Constancy

• Regular independent checks

The complementarity of the project - whether the project will be implemented without financing provided by carbon offset - determines the quality of the carbon offset credit. For this reason, currently carbon credits generated by renewable energy projects are losing out in price to other types of projects.

paid to monitoring processes related to GHG emissions.

2.3 Independent validation

The PDD validation procedure was well developed during the implementation of projects under the Clean Development Mechanism of the Kyoto Protocol. Audit companies accredited by the CDM Executive Board are also used for validation of offset projects.

During the validation process, the auditor must ensure that the project document has been prepared in accordance with the appropriate methodology and meets all the requirements of the standard. Upon completion of validation, a report is prepared indicating whether the project meets the requirements of the standard or not.

2.4 Project registration

The validation report with the auditor's conclusion is transmitted to the standard operator, who opens an account in the registry. The duration of the project's stay in the registry is usually 10 years. After all the preparatory work is completed, the physical implementation of the project begins. From the perspective of the carbon component of the project, the main attention should be paid to monitoring processes related to GHG emissions. Emissions monitoring is carried out in strict accordance with the Monitoring Plan, which is an integral part of the PDD. A monitoring report should be prepared at the end of each period. It is important that all monitoring results are documented, including the availability of certificates for the measuring equipment used. A qualified monitoring report with supporting documents is the key to success in monitoring.

2.6. Verification and introduction of emission reductions

Verification of emission reductions is a mandatory element of any international standard for carbon credits. Verification is carried out by independent audit companies that are part of the pool of a specific standard. As a rule, verifiers travel to the project implementation site to verify the reliability of the data presented in the monitoring report. Then, a verification report is being prepared with recommendations on the introduction of certain volumes of emission reduction into circulation.

Based on the verification report, the standard operator puts into circulation or issues certificates for each ton of emission reduction. Only after this procedure, the "virtual commodity" - GHG emissions - becomes a carbon offset credit with a specific name (commodity brand) and can be the subject of purchase/sale on voluntary carbon markets.

The received carbon offset credits are entered into the register of the standard at the account of their owner. Further, they can be stored, transferred, withdrawn from circulation/canceled when the credit is used to compensate for carbon emissions in some place.

2.7 How to Sell Carbon Credit

There are several options for finding potential buyers of carbon offset credits.

To organize the sale of their carbon credits, many project developers work with brokers. Brokers purchase offset credits and then transfer (or write off) them on behalf of clients. Some brokers sell offset credits from projects they have invested in, in addition to projects developed by others.

Another option is to sell carbon credits on the stock exchange. There are a number of environmental commodity exchanges, mainly in North America and Europe, that trade carbon offset credits and work with registries to ensure their transfer.

Some buyers of offset credits directly invest in a offset project in exchange for receiving the right to a portion of the credits generated by the project. This approach can provide deeper interaction and a more complete understanding of the strengths and weaknesses of the project.

As an option, it is possible to enter into a contract directly with the project developer in the form of an "Emissions Reduction Purchase Agreement" (ERPA). ERPA gives project developers confidence that they will be able to sell a reliable volume of offset credits. For buyers, the advantage lies in the ability to fix the price of credits in advance, which is usually lower than market prices (in exchange for some risk of delivery). ERPA can be structured in various ways, including in the form of option contracts.

Offset credits can also be sold through retailers. For buyers who want to receive only a small amount of offset credits (for example, for small companies or individuals), this is the most suitable option. In most cases, the retailer will keep records in the registers of carbon offset programs and withdraw offset credits from circulation directly on behalf of the buyer.

3. Example of selling carbon credits in a renewable energy project

Alibey Adasy Wind Power Plant (WPP), located in the Aegean region of Turkey, in Izmir province, was commissioned in 2018. The installed capacity of the plant is 30 MW, including four turbines with a capacity of 3 MW and five turbines with a capacity of 3.6 MW. The annual electricity generation is 111.66 GWh.

The total cost of the project is 34,094,662 euros, including capitalized financial costs and working capital requirements. The proposed financial scheme includes debt financing in the amount of 28,967,000 euros and the borrower's own contribution in the amount of 5,127,662 euros. The ratio of borrowed and own funds is approximately 85:15.

The estimated emission reduction was estimated at 58,000 tons of CO2-eq. per year. The project was registered with the Global Carbon Council (GCC) in 2020. The term of crediting or putting into circulation of carbon credits is 10 years. The price of 1 ton of carbon credit is equal to 5 US dollars. The additional revenue from the sale of carbon credits is estimated at approximately US$ 3 million.

Kazakhstan and World Bank discuss energy integration in Central Asia

Construction of 500 MW wind power plant begins in Karaganda region

50 MW solar power plant auction winner determined in Kazakhstan's Southern Grid Zone

Rooftop solar panels: Kyrgyzstan prepares rules for households and businesses

Europe’s rising heat: Can renewables provide the solution?

Winner announced for 100 MW solar auction in Kazakhstan

Chinese company ready to invest $1 billion in solar and wind generation in Kyrgyzstan

Meta to invest in space solar energy and ultra-long-duration energy storage

Tokyo pushing plan for world’s biggest floating wind power farm

Kazakhstan cancels 50 MW solar auction due to lack of participants

Tokayev ratifies Green Energy Corridor Agreement with Azerbaijan and Uzbekistan

China raises RES share to 60% of total installed capacity

Batys Kaspiy Energo wins auction for 250 MW wind farm in Atyrau region

Ember: Renewables overtake coal in global power generation for the first time

Kazakhstan continues accepting applications for May RES auctions

Water-energy balance of the region discussed by ministers of four Central Asian countries

Just transition: leaving no one behind in the energy transformation

CAREC and Central Asian universities sign new memoranda on green skills development

Kazakhstan and UNECE discuss energy resilience and low-carbon technologies

100,000 jobs and a skills gap: how Central Asia is preparing for the renewables boom