Expert opinion09.09.2022

A New Era in Decarbonization Policies: Carbon Border Adjustment Mechanism

Oğuz Tosun, Region Head – Turkey & MENA, EKI Energy Services Limited (EKI)

What will the CBAM dictate to Kazakhstan’s economy?

As the adverse impacts of the climate crisis are becoming more frequent every day, limiting the anthropogenic GHG emissions becomes more crucial. In this context, there is a strong decarbonization policy called carbon pricing. As carbon pricing becomes more effective, the carbon leakage risk brought together also becomes more visible for countries that implement carbon pricing measures. To prevent this economic threat along with aiming for climate action improvement globally, the EU has introduced the Carbon Border Adjustment Mechanism (a.k.a. CBAM) as part of the European Green Deal (a.k.a. EGD). For countries having a routed trading relationship with the EU, it is crucial to assess the potential impacts and the risks that will be imposed by the CBAM to their economies, especially for those that are not regulated by a carbon pricing instrument. As an example, for these countries, Kazakhstans’s economy is expected to be impacted by the CBAM whereas its environmental ambition likely increases.

Introduction

According to the World Bank (2020), anthropogenic activities across the world emit approximately 55 Gigatonnes CO2e of greenhouse gas (GHG) emissions to the atmosphere annually. Such an emission trend increased the atmospheric GHG emissions to 412.89 parts per million (ppm) which is drastically greater than the safest level for human civilization. Considering the consequences of this extraordinary atmospheric GHG concentration level (i.e., climate change), humanity has a significant liability to reduce the volume that is pumped into the atmosphere. In other words, people must decarbonize the way they live (i.e., the economy) a considerable extent as soon as possible. In this context, 64 carbon pricing instruments that are in force in different countries/ regions draw much attention with their ability to regulate the global GHG emissions by almost 23% (World Bank, 2020).

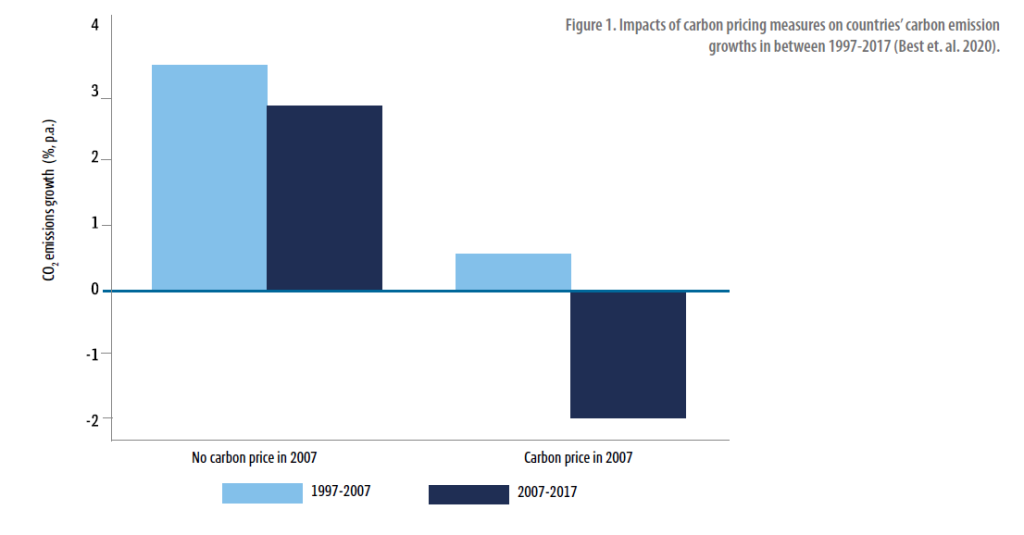

As shown in Figure 1, a recent published study has shown how carbon pricing instruments have facilitated the governments in slowing down their carbon emissions growth post-2007. According to the study, while the emission increase rate of the countries that do not apply a carbon price has decreased relatively between two decades, the carbon emission increase rate of the countries that do have decreased significantly.

EU ETS & Carbon Leakage Risk

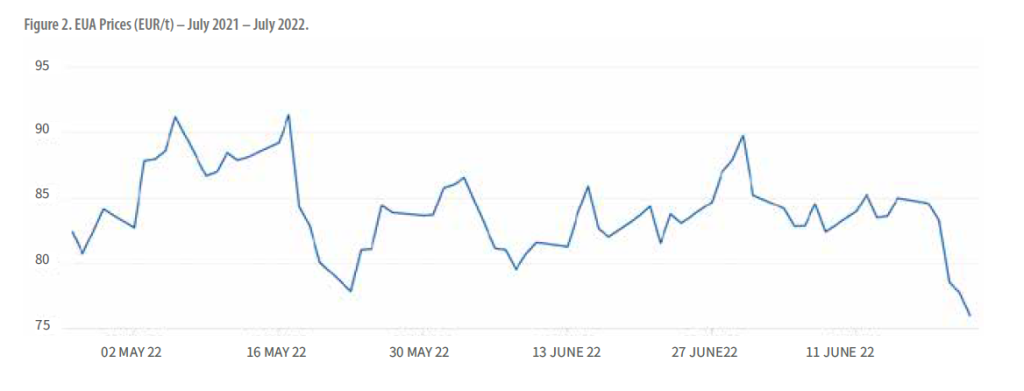

As the most experienced carbon pricing tool in the world, European Union Emissions Trading Scheme is one of the most successful one among all the carbon pricing instruments. For example, it covers 45% of EU emissions, its carbon unit European Union Allowance (EUA) has been transacted at a pricing level range of 77-96 EUR per tons of emissions between July 2021 and July 2022; collected more than EUR 80.7 billion revenue since its beginning (ICAP, 2022).

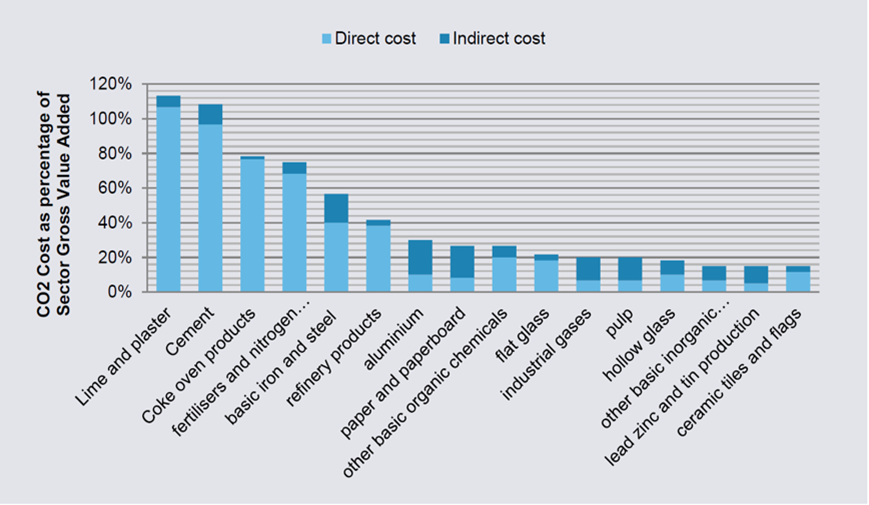

On the other, this successful carbon pricing brings an economic risk to the regulated sectors which is called carbon leakage. Carbon leakage refers to the risk of relocation of the headquarters of the companies regulated by a carbon pricing measure to a different country/region with laxer climate laws to avoid being subjected to carbon regulation (Tosun, 2019). In such a case, the emissions owned by these companies are not mitigated but occurred simply elsewhere (i.e., outside carbon border). For example, there are several sectors that are at risk of carbon leakage in EU borders, as shown in Figure 3. Thus jurisdictions like the European Commission adopts new policies to prevent this carbon leakage risk.

Figure 3. The sectors that are at risk of carbon leakage in EU ETS

There are two ways for allocating the emissions allowances (EUAs) to the polluters in the borders of the EU. The first one is allocating the allowance freely (i.e., grandfathering) whereas the second one is allocation of the allowance through auctions. In the second option, the jurisdiction basically gains carbon revenue from the regulated entities. Here a logical question would be like why to give the emissions permits to the polluters freely (i.e., grandfathering) rather selling them (i.e., auctioning). The answer arises from the carbon leakage risk. The EU ETS has completed its 3rd phase and started the 4th as of 2020. In the initial phases, in order to protect its industry players’ competitiveness against the owners of imports in EU borders, the EU has used this way of allocation of allowances. However, this application has brought some environmental and economic concerns together.

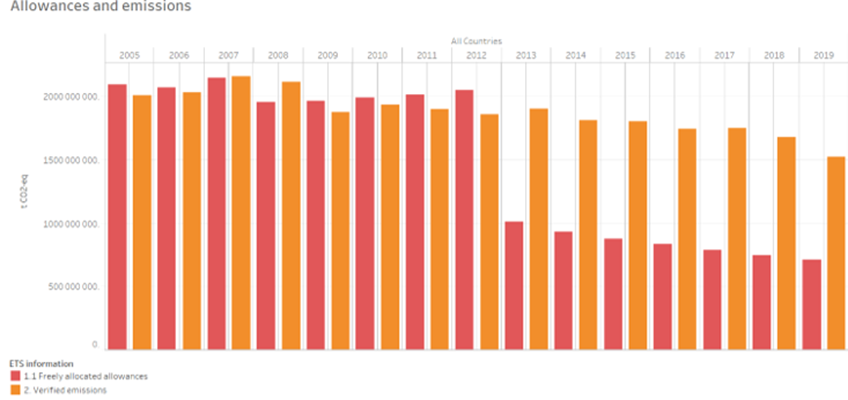

Figure 4 taken from European Environmental Agency (2020) shows the volume of the EUAs that are freely allocated, and the volumes of the verified emissions owned by the associated regulated sectors since the beginning of EU ETS. So, there are two main interpretations drawing attention with this figure. First, in the initial phases of the EU ETS, it is seen that the volume of the grandfathered allowances is greater than those verified emissions owned by the particular sector, which means EU ETS to lose a level of environmental integrity. Second, EU ETS has lost money on the allowances who were not auctioned but freely allocated. For example, a European NGO Carbon Market Watch has organized a campaign against the grandfathering by drawing attention to the extra money made by a regulated entity within the EU ETS (Figure 5). In response to these political concerns, the European Council (EC) has decided to adapt another and long-term way to deal with carbon leakage which is called Carbon Border Adjustment Mechanism (CBAM).

Figure 5. Counter argument against freely allocated allowances raised by CMW

Carbon Border Adjustment Mechanism

The Carbon Border Adjustment Mechanism idea is a climate policy not only meant to protect the industrial competitiveness of the EU industry players but also to foster the transition to climate neutrality by 2050. European Council has declared an agreement on the general approaches of the CBAM on 15 March 2022. With this new carbon pricing measure, the non-EU companies who are not regulated or regulated less by a carbon pricing instrument (e.g., carbon tax or cap and trade) in their origin countries will be (further) regulated by a border carbon taxation for their exports from particular industries such as “Iron&Steel, Cement, Fertilizers, Aluminum and Electricity” by the European Council.

Since the first official rumors on the CBAM were first heard, many technical issues came into discussion tables across the Europe and in its top trading partners. Major issues are addressed in Table 1 as per the expectation raised before the declaration of the agreement.

Table 1. Clarifications given in the CBAM Agreement

|

Issue |

Clarification given in the agreement |

Next steps |

|

Mode of Pricing |

Mirror of EU ETS |

Not expected. |

|

Sectorial Scope |

The products of the following sectors will be covered by CBAM: cement, aluminum, fertilizers, electric energy production, iron and steel |

It is expected that the CBAM will be extended to cover all EU-ETS sectors in the coming compliance periods. |

|

Emissions Scope |

Only Scope-1 emissions of (i.e., consumption of heat/cooling and on-site electricity production) will be covered. |

It is expected that Scope-2 emissions will be covered in the coming compliance periods. However, either technical or political serious thoughts have not been aired on Scope-3 emissions coverage yet. |

|

Governance |

Centralized registry run by the European Commission |

None |

|

Nature of commodity |

CBAM certificates issued by the European Commission |

It is expected that the CBAM certificate will be directly linked to EUA in terms of financials and legal nature by the first compliance period. |

|

Reporting Requirement |

Puts serious liability on the European Commission |

The Commission shall publish official views on the future implications of the CBAM regulation with an inclusion on sectorial, scope related extension for a better addressing of carbon leakage. First official evaluation by the Commission shall be published before 1 Jan 2026; new reports shall be published every two years. |

|

Exemptions |

On consignment rates only |

European Council expects a minimum threshold which exempts from the CBAM obligations consignments with a value of less than €150. Decision on another potential exemptions based on different criteria such as geographical exclusions (i.e., exempting the exports from LDC) shall be made in the coming compliance periods. |

|

Avoidance of EUA Grandfathering |

Missing |

Stopping allocating the allowance freely is one of the major expectations from the CBAM. The Commission needs to publish a rigid timeline to phase out the grandfathering era. |

|

Export Rebates |

Missing |

No clarification has been published the alignment to World Trade Organization’s principles and rules. The Commission needs to address an avoidance policy for export rebates in the new pricing scheme. |

|

Revenue Use |

Missing |

No clarification has been published for the use of the carbon revenue that will be gained from the CBAM. The Commission shall publish a rigid framework for the beneficiary groups of the CBAM revenue. For instance, WWF calls for CBAM revenues to be returned to developing countries in the form of international climate finance. |

The EU has two fundamental purposes behind the implementation of the CBAM. While the first one is to protect the European industry players’ competitiveness from the economic impacts of carbon leakage, the second one is to enhance the climate action beyond EU borders by incentivizing the decarbonization policies via market-based instruments. Moreover, with the CBAM, it is also aimed to foster global climate action to make the global economy in line with the Paris Agreement.

Case Study: The CBAM & Kazakhstan - Magnitude of Exposure

Qazaq economy will be one of those countries that will be impacted by the upcoming CBAM referring the aggregated European import volume from Kazakhstan, recorded as US$20.51 Billion. Table 2 shows the volume of the export activity from various Qazaq industries to EU. Addressing this figure, developments on implementation of a carbon border adjustment mechanism by EU shall draw the attentions from its trading partners such as Kazakhstan. Although the Qazaq economy is regulated by a national emissions trading scheme, the Qazaq ETS’ ambition level is not well enough to prevent from adverse economic impacts of the EU CBAM. Thus, its competitiveness for EU exports is at risk against its rivals in the list.

Table 2. European Union Imports from Kazakhstan

|

Industry |

Export Volume |

|

Mineral fuels, oils, distillation products |

$18.67B |

|

Inorganic chemicals, precious metal compound, isotope |

$387.43M |

|

Copper |

$318.86M |

|

Iron and steel |

$255.00M |

|

Oil seed, oleagic fruits, grain, seed, fruits |

$208.34M |

|

Aluminum |

$176.19M |

|

Pearls, precious stones, metals, coins |

$101.97M |

|

Cereals |

$54.21M |

|

Others |

$336.37 M |

recent study by The Task Force on Climate, Development and International Monetary Fund (TCD-IMF) reveals the economic exposure level owned by Kazakhstan against the CBAM. The study considers Kazakhstan’s 2026 greenhouse gas emission inventory projection data and the and different pricing scenarios of EU ETS which is given in Table 3:

Table 3. CBAM Scenarios

|

Scenario |

Description |

|

1 |

Only direct emissions (Scope 1) from the production of imported goods are used to calculate the carbon embodied in the imports |

|

2 |

All imported goods and services, and all indirect emissions from upstream value chains (Scope 3) are included in calculating the carbon contents |

Addressing these scenarios, Qazaq economy’s magnitude of exposure by the EU CBAM with respect to several parameters are summarized in Table 4.

Table 4. The Impact of the CBAM with respect to different parameters and scenarios

|

Parameter |

Unit |

Magnitude of Exposure |

|

|

Scenario 1 |

Scenario 2 |

||

|

Impact on Exports of CBAM Products to the EU |

% from baseline, 2030 |

-1.4 |

-46.8 |

|

Impact on GDP |

% from baseline, 2030 |

-1.4 |

-46.8 |

|

Change in Welfare from Baseline |

in USD bn, 2030 |

-0.2 |

-9.0 |

Another interpretation of the study by the United Nation Conference on Trade and Development (UNCTAD) addresses how the CBAM enhance the environmental integrity of Kazakhstan’s economy. The study says that the national greenhouse gas emission can decrease by 0.83% in case the CBAM is implemented where EUA is transacted at 44 USD/t and %1.24 where EUA is transacted at 88 USD/t. In this respect, the question that shall be raised by the respective Qazaq regulatory authorities is how to achieve this minimum climate ambition by circulating the same amount of carbon revenue in the borders of Kazakhstan by avoiding the potential financial outflows to European industry competitors.

Conclusions

When it comes to carbon pricing, there are always some arguments that assert it is actually a danger for the particular economies. However, in the era of the new climate regime which will be dictated by the contemporary climate regulations such as the Carbon Border Adjustment Mechanism as part of the European Green Deal (EGD), actually such anti-carbon regulation arguments are not good for the economy neither at national nor international level. Countries like Kazakhstan that implements weak carbon regulations need to prepare themselves to the requirements of the new climate regime which will be possibly dictated by several overseas climate actions. Although Kazakhstan has already taken the first step to respond to the EU CBAM, its economy is still at risk against the rocket carbon prices owned by its trade partners such as European Union and many others that are in preparation for their own border carbon regulation instruments such as China or USA. Indeed, as also seen in Table 3, it can be easily understood that adapting emerging economies like Kazakhstan’s to the EGD is cheaper than being regulated under it. Thus, preparing for the potential risks of the Carbon Border Adjustment Mechanism by firstly enhancing the existing Qazaq ETS can be a good start. The best strategy in the medium term then will be introducing an economy wide carbon pricing regulation where many industries are regulated for all three scopes of emissions at fair at environmentally competitive carbon prices to deal with the implications of the new climate regime best.

Germany adds more than 1 GW of offshore wind capacity in H1 2026

LONGi sets new world record with 35.5% efficient silicon-perovskite tandem solar cell

Albania allows renewables on agricultural land

EU unveils reform of ETS and Electrification Action Plan

Kazakhstan plans to add more than 26 GW of new power generation capacity by 2035

Energy origami: Austrian engineers teach solar panels to hide from hail

Rimini to host Ecomondo 2026 — Europe's top platform for sustainable technologies

DHL, Statkraft ink 10-year wind power deal

China's energy transition: from a gigawatt race to market efficiency

Solar power supplied a quarter of EU electricity for the first time in June

Kazakhstan's Energy Ministry and EBRD discuss development of just energy transition partnership

Kazakhstan generated 63.4 billion kWh of electricity in H1 2026

Samruk-Energy and SANY Renewable Energy sign shareholders' agreement for 1 GW wind project

IRENA: Renewables generated 31.7% of global electricity in 2024

EU approves funding for 11 offshore wind farms in France

Chinese scientists propose laser power network to supply lunar rovers with wireless energy

Ocean Winds brings France's first floating offshore wind farm to full power

India installs record 26 GW of solar and 2.9 GW of wind capacity in H1 2026

Poland's first offshore wind farm delivers electricity to the national grid

Ainur Sospanova elected chair of the new sectoral council on renewable energy